At Dimerco’s 2026 Annual Management Meeting, Bronson Hsieh, former Chairman of both Evergreen and Yang Ming, outlined the factors driving change across the ocean freight market this year.

The market is being shaped by a mix of policy changes, shifting trade flows, capacity adjustments, and ongoing disruption.

For shippers heading into 2027, that makes planning more complicated. Conditions are no longer consistent across trade lanes, and many of the assumptions that used to guide procurement decisions are starting to break down.

Hsieh sees the real challenge as understanding what’s driving these changes.

A closer look at how this is shaping 2026 planning is in the full briefing.

A More Stable Economy Than Expected

Looking at the broader backdrop, the global economy is holding up better than many expected.

Forecasts for 2026 show modest year-over-year growth across major economies.

The U.S. is projected at around 2.4%, China around 4.5%, and Europe near 1.3%, based on IMF estimates.

It is not a high-growth environment, but it is stable enough to support trade. Demand has not disappeared. It has shifted.

For shippers, the issue is not weak demand, but where demand is showing up.

Tariffs Are Still Driving Decisions

The U.S. continues to adjust tariff measures across key trading partners, with changes introduced in early 2026 affecting both country-specific and product-specific imports.

Enforcement has also tightened. Shipments routed through third countries to avoid China tariffs are facing greater scrutiny, particularly across parts of Southeast Asia. In some cases, reclassified cargo or unclear origin documentation is leading to significantly higher duties.

Smaller shipments are also affected. The U.S. has removed de minimis eligibility for many low-value imports, meaning shipments that previously entered duty-free are now subject to tariffs. This has changed the cost structure for cross-border e-commerce.

Policy is still moving quickly. Tariff levels, enforcement practices, and eligibility rules are being updated as trade negotiations and political priorities evolve.

For shippers, that makes fixed sourcing strategies harder to rely on. Routing and supplier decisions now carry more risk, especially in lanes exposed to policy changes.

Front-Loading Is Still Distorting the Market

One of the biggest drivers of current conditions is timing.

In early 2025, importers accelerated shipments ahead of expected tariff increases. Volumes rose sharply in the first quarter, then softened later in the year.

That shift is still affecting how demand looks today. Early 2026 numbers may appear weaker, but they are being compared against an unusually strong period.

U.S. Import Demand Is Uneven

Cargo flows into the U.S. are no longer consistent.

Far East to U.S. volumes increased early in 2025, then declined later in the year, ending slightly negative overall.

Forecasts show softer volumes in the early part of 2026, followed by a recovery later in the year as inventory is replenished.

Demand is still there. What has changed is when and how companies are buying.

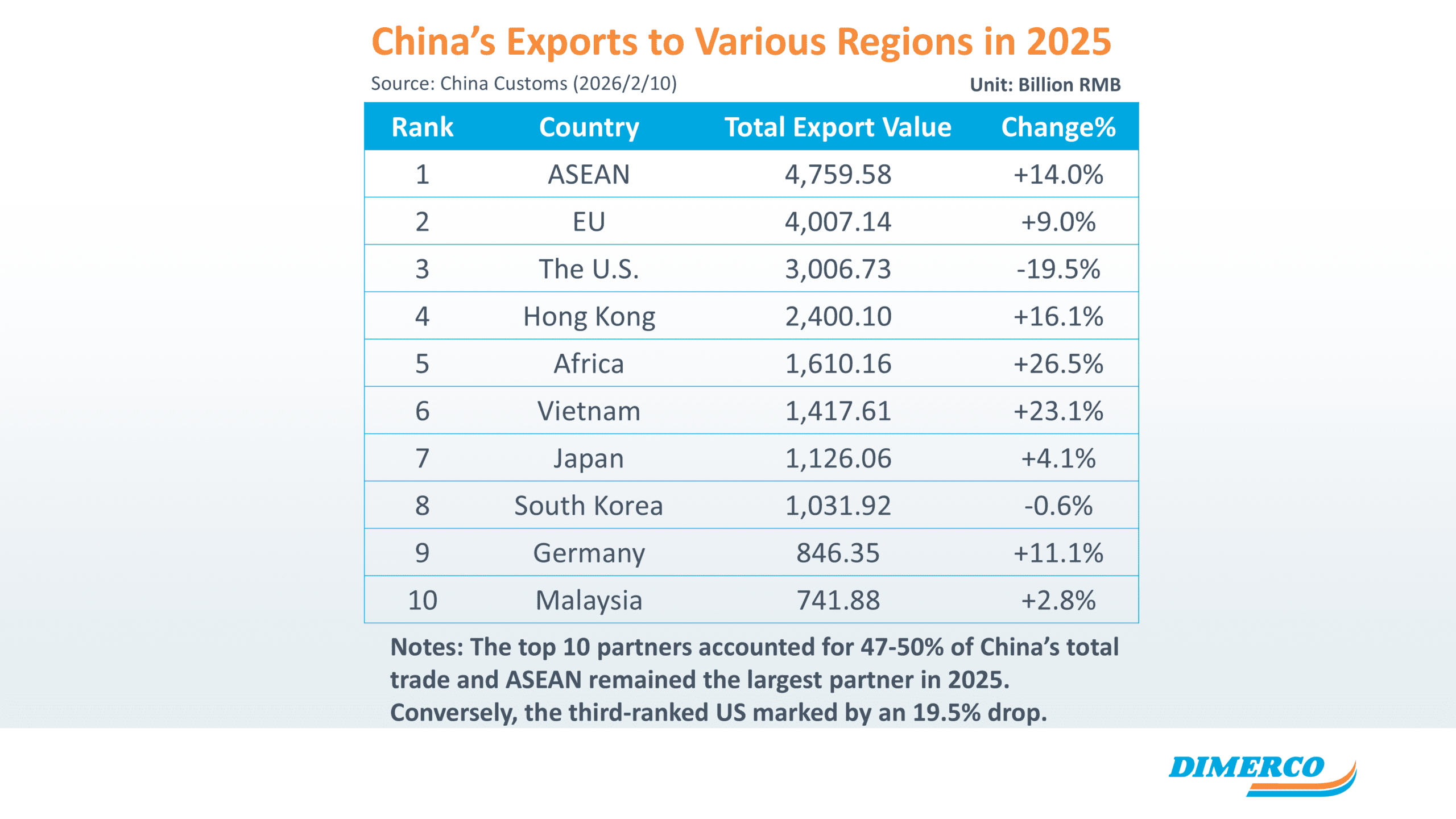

Trade Is Shifting, Not Slowing

Global trade volumes are still moving, but the direction is changing.

China’s exports to the U.S. declined by roughly 19.5% in 2025. Over the same period, exports to ASEAN increased by 14%, exports to Europe rose by about 9%, and exports to Africa grew more than 25%.

China’s total container throughput still grew, reaching over 324 million TEUs.

The volume is still there, but it is moving to different regions.

Southeast Asia Has Become a Core Hub

Southeast Asia is now central to supply chain strategy.

Production is shifting into the region as companies look to reduce tariff exposure and diversify sourcing.

This has led to steady export growth and continued investment in port infrastructure across countries like Vietnam, Indonesia, Malaysia, and Thailand. Major hubs such as Tanjung Pelepas and Laem Chabang continue to expand as volumes increase.

Shipping lines are increasing capacity into these markets to support that growth.

Capacity Looks Ample, But It Is Not Evenly Distributed

Fleet growth suggests more capacity is entering the market.

New vessel deliveries are increasing supply through 2026 and beyond.

That capacity is not evenly distributed across trade lanes.

Routes outside the U.S., particularly into Europe, Africa, and Latin America, are seeing stronger capacity growth as carriers adjust deployment away from traditional U.S.-focused lanes.

The Red Sea is still a Key Variable

The Red Sea situation continues to affect capacity.

As Bronson pointed out, rerouting vessels around the Cape of Good Hope has reduced effective global capacity by roughly 9%.

The exact impact continues to fluctuate depending on routing decisions and security conditions in the region.

If conditions change and vessels return to Suez, that capacity could come back into the market quickly.

This remains one of the biggest unknowns for both pricing and service planning.

Carriers Are Managing Capacity More Actively

Carriers are adjusting how they operate. They are controlling supply through:

- Blank sailings

- Slower sailing speeds

- Network adjustments

These actions help balance supply with demand and reduce volatility.

Reliability Is Becoming More Important

Schedule reliability is improving across some services.

Gemini cooperation services, for example, have reported reliability levels close to 90%, showing how carriers are prioritizing schedule consistency.

More consistent transit times help reduce delays and inventory risk.

For shippers, this becomes part of the cost equation, not just a service metric.

What Shippers Should Take From This

Several themes are coming through as the market continues to shift.

Trade policy is still moving faster than most supply chains are built to react. Tariffs, enforcement changes, and sourcing decisions are all happening at the same time, often without clear timelines.

Demand is not disappearing, but it is becoming less predictable. Timing, routing, and inventory decisions now carry more weight, especially as front-loading and policy changes continue to distort typical patterns.

Supply and capacity are not evenly aligned. Carriers are adjusting networks, and disruptions like the Red Sea situation are still affecting how capacity flows through the market.

For shippers, this means planning cannot rely on a single assumption. Flexibility across sourcing, routing, and contract structure is becoming more important.

If you are navigating tariff exposure, changing trade lanes, or upcoming contract negotiations, get in touch with a Dimerco specialist to discuss how these developments may affect your supply chain planning.